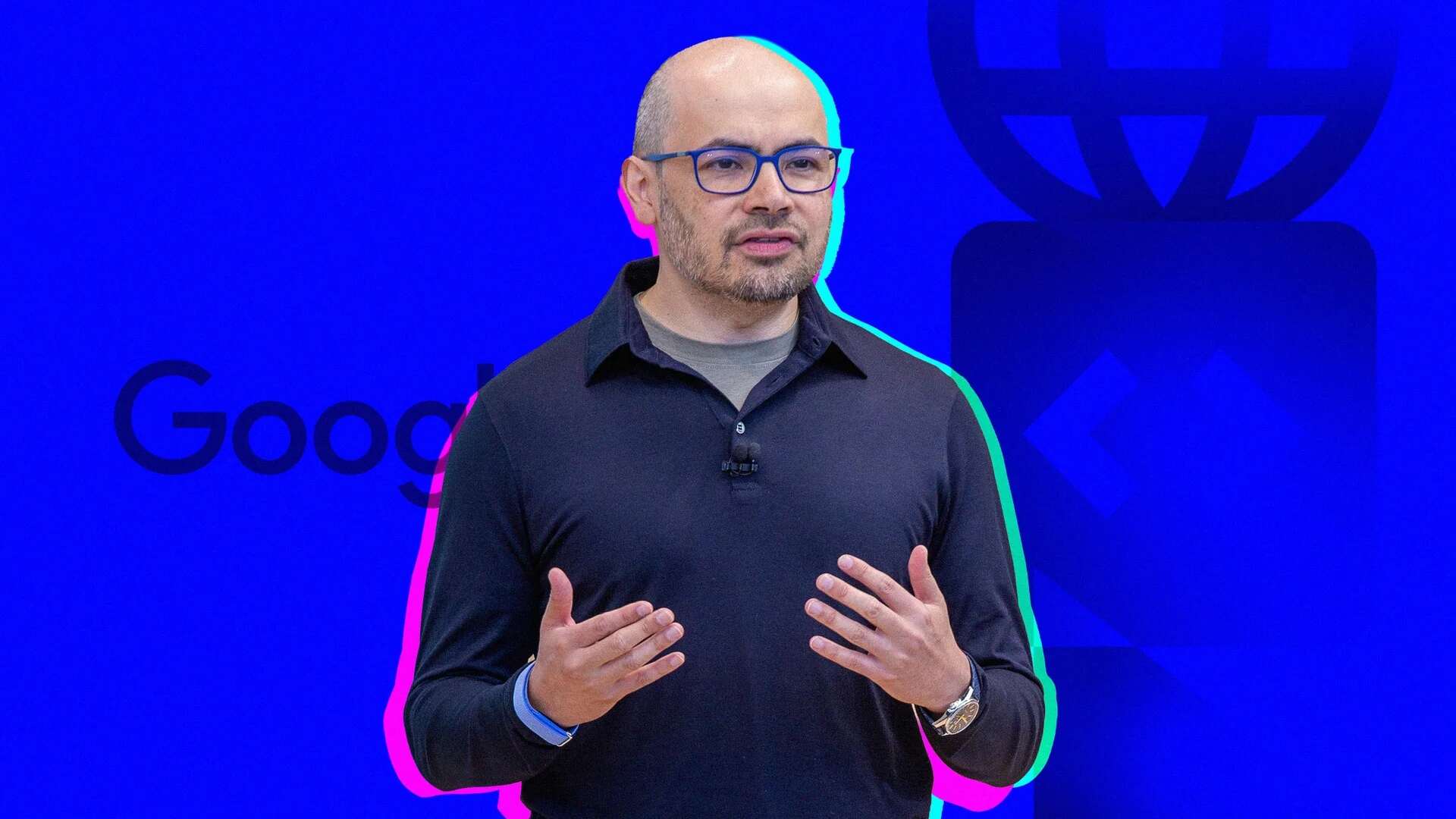

- | 9:00 am

Fintech will meet the needs of the unbanked, says Khalifa Al Shamsi

In an exclusive interview, Khalifa Al Shamsi, CEO of e& life, talks about how advancing fintech solutions can lead to financial inclusion and spur a cashless economy.

Despite fintech’s significant strides in the Middle East, a vast population remains unbanked. The traditional financial banks may have failed to build inclusive solutions, and the credit system doesn’t work for the millions of underbanked. This has created a space for innovative fintech players to disrupt the current financial system.

A new entrant, albeit a heavyweight, is UAE’s telecom giant Etisalat Group, which rebranded as a technology and investment conglomerate, e&. The group rolled out several fintech initiatives as part of its diversified business approach to offer “powerful, seamless digital experiences” to customers and empower digital society.

Behind this pivot is a man who has seen the evolution of the UAE’s digital landscape. With a pulse on the prime fintech opportunities and the challenges holding back the industry, Khalifa Al Shamsi, CEO of e& life, a business pillar carved out under e&, says the shift is a natural transition to serve the fast-growing sector.

“Go forth and conquer,” Al Shamsi says, is the group’s strategy in the coming months. “The UAE market, with more than 80% mobile penetration, and Etisalat’s strong customer base, are other strengths the group will be leveraging.”

TARGETING THE BANKED, UNDERBANKED AND UNBANKED

Al Shamsi says the company looks at banked, underbanked, and unbanked. “One of the most important aspects of e& money (the fintech arm of e& life and a rebrand from eWallet) is financial inclusion as we advance fintech solutions that make a difference in customers’ lives by delivering an innovative end-to-end financial marketplace that meets their financial needs,” he says.

Despite the ubiquity of mobile money, some people aren’t yet ready to give up coins and notes. Currently, 55% of payments are made in cash in the UAE. Although the reasons for this vary, Al Shamsi foresees fast-paced flight from cash due to convenience. “e& money makes it easier for the unbanked to use services that they would otherwise struggle to access.”

“It enhances the customer experience and enables them to do their financial transactions seamlessly, conveniently, and securely. This will spur a cashless economy.

“We want e& money to be a comprehensive financial services marketplace so that whenever people think of any money-related activity, they will think of e& money,” says Al Shamsi.

Al Shamsi explains how e& money will cater to all, “We are building a comprehensive platform by enabling partnerships specializing in payments, wealth management, remittances, insurance, open banking, buy now, pay later, and lending.”

Growth and restructuring go hand-in-hand. Al Shamsi explains that the telecom group has a multi-level approach to digital opportunities, and e& life is “a specialist business pillar” transforming into a global technology and investment conglomerate. He says its creation resulted from the “realignment of the business operations and the emergence of a diversified business model” to offer customers robust, seamless digital experiences and empower digital society.

Taking stock of the fintech industry’s accelerated growth in the region, he says, “Ramping up our fintech propositions is based on the rapidly changing consumer payment behavior, with many adopting contactless payments.”

ADDRESSING CUSTOMERS’ FINANCIAL NEEDS

In the fast-evolving fintech industry, when consumers and merchants seek an integrated financial marketplace to simplify transactions, e& money, the first wallet licensed by the Central Bank of the UAE, addresses various financial needs. “We have enriched the product portfolio of the e& money app with financial services ranging from merchant payments to insurance services,” says Al Shamsi.

“It is becoming a comprehensive super app that addresses a variety of customers’ financial needs, giving them access to financial services such as merchant payments, money remittances, bill payments, lending, investments, network branded cards, and insurance services.”

AI IS THE GLUE

The convergence between AI and fintech is huge, and Al Shamsi says it’s revitalizing the industry. The e& money super app marketplace provides consumers with AI-based platforms, credit scoring algorithms, and advanced analytics platforms. “AI helps us understand consumers’ needs to provide them with the right communications and create offerings that best meet their requirements,” he says, adding that AI will streamline the customer delivery process as it is the “ideal tool to understand rapidly-evolving demands and payment behavior.”

Speaking of the financial app, he says, AI is the glue that holds it together, “AI kicks in at the moment of registration and login, with facial recognition. On the advanced analytics side, AI allows us to segment users better and tap into data useful for credit scoring. For instance, buy now, pay later requires a lot of AI-powered analytics.”

Recognizing the risks that come with fintech, he adds, that the group relies on AI to prevent fraud.

THE FUTURE IS FINTECH

The ongoing transition within the group reflects the role played by digitization in creating a financially inclusive society and economy. While digitization marks a paradigm shift for major sectors, many dormant opportunities exist. Al Shamsi is placing his bets on fintech innovation as a top trend in the region. “We look forward to being a key player in this arena,” he says.

A technology he is vouching for is blockchain, which he says will continue to rise due to its capability to mitigate fraud risks. “Transactions can also be traced easily and in an immutable manner.”

“AI and Machine Learning will also be adopted more widely in the banking sector through a 24/7 self-service model,” he says. In the banking sector, he adds, AI will be used for cost-optimization (conversational banking), middle office (fraud detection and risk management), and back office (underwriting).

Although the first half of 2022 has been bad for the crypto market, he predicts that the adoption of crypto card payments and cryptocurrencies will increase. “There will also be a wider push for Central Bank Digital Currencies.”

As the interview draws to a close, we ask him about the group’s expansion plans for the next five years. He says, “We are ready to scale the fintech business line as we possess a large customer base that offers scalability and quick take-up. We have access to rich data for advanced analytics, differentiating technologies and design capabilities. We have enhanced customer experiences through our brick-and-mortar outlets and 24/7 accessibility to our customer care.”

Apart from fintech, the group aims to leverage the success it had with E-Vision to build a specialized media company. Despite the increased regional competition, the market, he says, is not saturated, and media penetration is still in its infancy. “We will adopt a 360-degree media and entertainment business in multimedia approach, which will be achieved through E-Vision.”

“We want to transform our entertainment streaming division into the super content and multimedia aggregator for the MENAP region and Western Africa — through a suite of solid video and audio offerings — from original local content and live sports to exclusive music, podcasts, and live audio.”

There is, however, still a long way to go before many of these are realized. Al Shamsi says, open to exploring untapped avenues, “some of the growth will be organic, some will be collaborative, but other growth opportunities may come through acquisitions.”

Most Innovative Companies comes to the Middle East this October! Click here to know more.