- | 12:00 pm

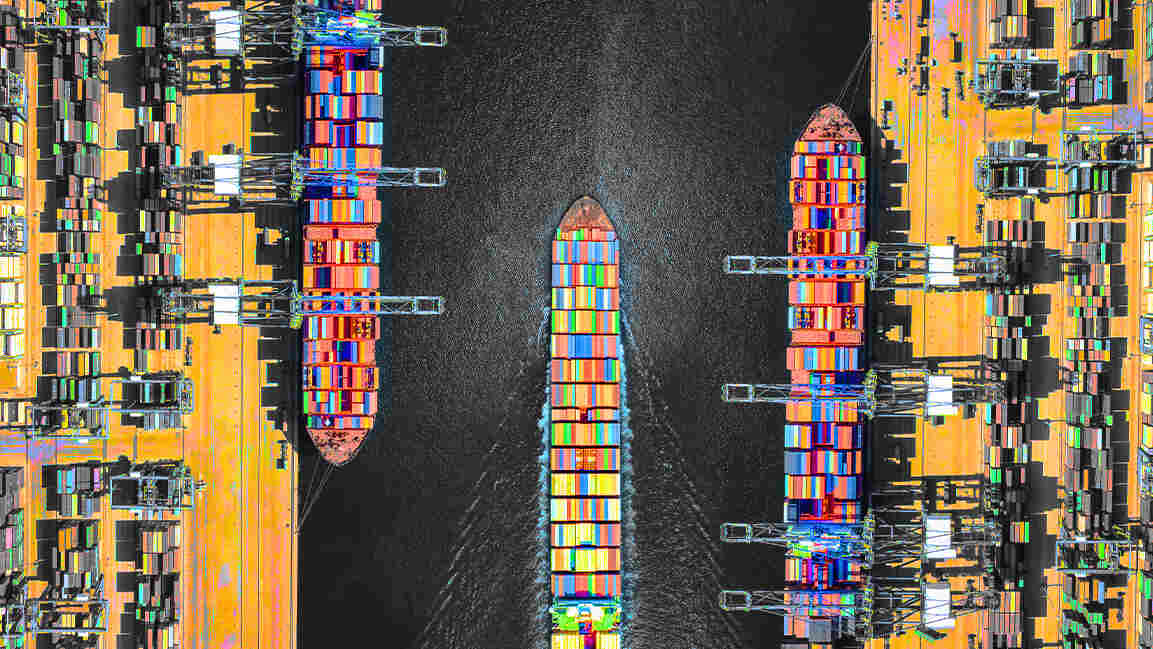

The $20 million-barrel question: How port disruption and risk at Hormuz affect global trade

When chokepoints tighten and ports stall, resilience becomes the world’s most valuable commodity.

Global trade doesn’t usually break all at once. It bends. It reroutes. It reprices risk. However, when labour disruptions at major ports coincide with escalating instability in the Strait of Hormuz, the system does not merely bend. It constricts.

The Strait of Hormuz carries roughly 20% of global oil consumption and about one-fifth of global LNG trade, according to the U.S. Energy Information Administration and reporting by Reuters. Analysts cited by The Guardian warn that any sustained disruption could drive oil prices sharply higher, amplifying inflationary pressure across transport, food, and manufacturing.

At the same time, recent port strikes in major global hubs, covered extensively by Financial Times and The Wall Street Journal, show how quickly supply chains seize when even a single node stops functioning. Individually, these events can cause severe disruption. Together, they expose an uncomfortable reality: global trade remains structurally vulnerable when key checkpoints are stressed.

Geopolitics Is No Longer a “Premium”

The corporate mindset has shifted. Nicolas Michelon, Managing Partner at Alagan Partners, observes that governments and multinational firms are abandoning the notion of treating geopolitical risk as an abstract premium and instead embedding it as a fixed operational cost. “Governments and multinational firms are moving away from treating geopolitical risk as an abstract premium and are instead embedding it as a core, fixed operational cost,” he says. For companies operating in the GCC, this shift often means moving from lean, just-in-time logistics to just-in-case approaches and holding three to six months of critical inventory locally.

Insurance has also become a strategy. War-risk premiums in the Gulf have risen sharply during recent escalations, according to international market reporting. In response, large firms are turning to captive insurance structures or even sovereign guarantees to keep trade lanes operational when private insurers hesitate.

At the government level, Gulf states are pursuing a careful diplomatic balance, maintaining security partnerships with the United States while preserving economic and diplomatic channels with China and Russia so that non-energy trade, such as food, medicine and other essential goods, remains insulated from geopolitical spillover. This is not merely reactive crisis management; it is systemic hedging.

The Double-Chokepoint Problem

The threat is not limited to the Strait of Hormuz.

Michelon describes a “double-chokepoint trap”: instability around the Strait of Hormuz coinciding with disruptions in the Red Sea and Suez Canal corridor. Attacks on commercial vessels in the Red Sea have already forced rerouting, as reported by Bloomberg and Reuters.

When both corridors are threatened, the only viable alternative for Asia–Europe shipping is around the Cape of Good Hope, a detour that, during previous disruptions, added roughly 20–25 days to transit times and significantly increased fuel and crew costs, according to shipping data reported by Bloomberg.

Longer routes reduce available vessel capacity, which pushes freight rates higher and transmits further inflationary pressure through global supply chains. If port strikes simultaneously diminish handling capacity at key hubs, congestion and delay compound rapidly.

The Real Risk: Energy Absence

Market commentary tends to focus on oil prices, but they are only part of the story. Brent crude has recently traded in the $70 to $80 range, yet analysts warn that a prolonged closure of the Strait of Hormuz could drive prices materially higher. Michelon emphasizes a different danger: quantity, not merely price.

Approximately 20 million barrels per day transit Hormuz, and global spare capacity to replace that volume is limited. A disruption lasting four to five weeks could force industrial slowdowns in major importers such as China and India. “The biggest risk for the world economy is not so much the price of the crude oil barrel,” he says, “as it is the absence of energy to power Asia’s industrial powerhouse.” Energy scarcity not only raises costs but it halts production.

The Gulf is also a significant exporter of fertilisers, including urea and ammonia. Energy constraints or export bottlenecks could therefore affect agriculture and trigger secondary food price pressures over subsequent months. In this context, Michelon describes a prolonged closure of the Strait of Hormuz as an event that could precipitate a synchronized global recession, not solely because of volatility, but also because of systemic constraints.

Inside the Corporate War Room

For companies based in the United Arab Emirates, the priorities shift quickly from macroeconomic analysis to duty of care. Sébastien Bedu, General Manager Middle East at International SOS, argues that organisations must escalate from routine operations to crisis readiness in a swift, coordinated manner grounded in verified information. With periodic airspace closures, flight suspensions and mobility constraints affecting the region, UAE-based organisations must protect both business continuity and employee safety. “Effective leadership acts as a stabilising force,” he says. That leadership requires a centralised executive voice, fact-based communications and active measures to filter misinformation.

Some practical steps are essential. Organisations should have formal business continuity plans ready for activation, established partnerships with trusted security and medical providers, real-time staff accountability systems and contingency measures that anticipate aviation disruption and border congestion. If shelter-in-place directives are issued, plans must allow employees to remain self-sufficient for 48 to 72 hours while receiving both practical and emotional support. In this environment, resilience is both procedural and strategic.

Pipelines in Saudi Arabia and the UAE provide partial bypass capacity, yet regional pipeline infrastructure cannot replicate the roughly 20 million barrels per day that transit the Strait of Hormuz. Pipelines can alleviate pressure, but they cannot substitute for the strait’s throughput. This quantitative reality highlights why the strait remains one of the most consequential energy chokepoints in the world.

The Competitive Edge Is Preparedness

Preparedness is a competitive advantage. For companies across the Middle East, this is a moment for posture, not panic. Geopolitical risk must be built into operating models. Inventory buffers, alternative routes, sovereign-backed insurance and tested crisis plans now separate firms that can keep trading from those that cannot. The question is no longer whether disruptions will occur but whether organisations can keep operating when they do. In a world channelled through narrow corridors and synchronized logistics, resilience is strategic.

Featured Videos

More Top Stories:

FROM OUR PARTNERS